Article

Scaling Storage: Fire Risk, Supply Chains and the Next Wave of BESS Innovation

24 March, 2026

By : Michael Carrington,

Underwriter, Tokio Marine GX

Two years on from Tokio Marine GX’s Batteries Not Excluded report, Battery Energy Storage Systems (BESS) have truly become a focal point for global clean energy investment – now representing a significant and growing proportion of our total insured portfolio across Europe, the U.S. and Asia.

We speak to Michael Carrington, Underwriter at TMGX, who has recently attended two of the most important energy storage events of the year: the Energy Storage Summit and the Investing in Battery Energy Storage Conference (IBES).

In our Q&A, we discuss the importance of large-scale fire testing, how U.S. and European manufacturers, owners and operators can reduce their supply chain dependency through industry innovation, and the key challenges both mature and new BESS markets are facing.

• What are your key takeaways from recent industry conferences?

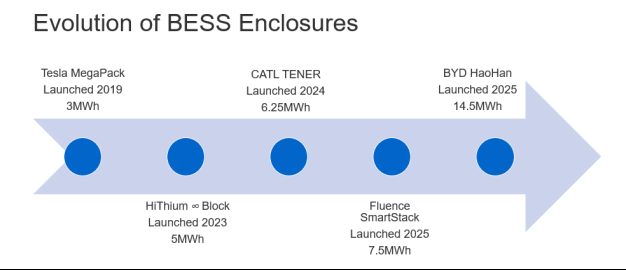

It’s clear that the BESS industry is seeing a step change in the size of individual battery enclosures and the technology that underpins them. BESS OEMs have responded to market demand for greater energy capacity and in a short timeframe, have shifted to enclosures capable of delivering megawatt-hours many multiples higher than those launched just a few years ago. This change is illustrated in the slide below.

It’s great to see so much R&I go into the battery sector, but as insurers, we will always be cautious of the rate of innovation and the lack of operational track record for new technologies.

This step change isn’t confined to BESS; the rapid and constant development of new renewables generation technology, such as ever-growing wind turbines, have posed challenges for insurers in the past. No one wants to underwrite a project with a blindfold on...

Technology venturing into unknown (or untested) territory significantly increases the risk profile of a BESS project, with knock-on effects for its insurability and bankability.

Industry standards have been working to keep pace with the rate of technology innovation. One critical procedure that has emerged is Large-Scale Fire Testing (LSFT). This addresses the limitations of the UL9540A testing method and gives owners, operators and insurers greater insight into the real-life onsite exposures presented by a BESS enclosure. Prospective insureds looking to adopt BESS technology that has undergone successful Large-Scale Fire Testing are likely to increase the insurability of their project.

A number of OEMs globallyhave already invested in LSFT of their BESS solutions. Given the congested BESS marketplace, those manufacturers looking to distinguish themselves and their products are those undergoing the Large-Scale Fire Test procedures. This enhanced level of testing and transparency from OEMs to share the testing reports will be welcomed by insurers. In the U.S., the 2026 edition of the NFPA 855 Standard has been updated to include LSFT as a mandatory requirement and we expect other jurisdictions to adopt this as best practice guidance.

- Our Batteries Not Excluded report in early 2024 highlighted supply chain issues as a key challenge for the industry – is this still the case?

Unfortunately, yes. A significant part of this bottleneck is caused by the European and U.S. markets’ dependence on Chinese BESS technology, which continues, two years on.

I had some interesting conversations at the Energy Storage Summit and IBES about how the industry might reduce its reliance on a single source, and Sodium-Ion batteries (SIBs) were mentioned time and time again.

This technology won’t replace Lithium Iron Phosphate (LFP) chemistry, for which most of the materials come from China. However, sodium-ion batteries present an exciting new alternative that does not depend so heavily on cross-border supply chains, as they are built with largely abundant materials, like sodium and aluminium (rather than lithium or nickel and cobalt in the case of NMC chemistry). Some of these batteries are already being produced in the U.S. and within the European Union.

From a risk management perspective, there are multiple benefits to using sodium-ion batteries instead of LFP:

- Safety Benefits: Early research suggests that sodium-ion batteries offer higher thermal stability, making it harder to trigger thermal runaway events compared to LFP. Similarly, they can withstand more extreme temperature conditions than LFP and have better puncture and impact resistance than other batteries.

- Operating Costs: SIBs can be cooled entirely by passive means, which greatly reduces operating costs.

- Manufacturing Synergy: Existing facilities fabricating LFP-powered batteries can be adapted for sodium-ion production with only minor adjustments, therefore not requiring significant amounts of investment.

- Reduced Geopolitical Risks: The materials needed carry significantly lower geopolitical and supply-chain risks associated with mining, sourcing, and price volatility. Plus, being able to build them domestically means the batteries may avoid heavy tariffs.

An initial downside of sodium-ion technology is, again, connected to its nascency and limited track record on a utility storage scale. As I mentioned, such BESS solutions can increase their insurability through the adoption of Large-Scale Fire Testing, clearing the path of uncertainty and allowing insurers to confidently underwrite these projects with a better understanding of the exposure.

TMGX has been monitoring SIBs for some time and are well positioned to support this next evolution of projects when they come to market.

- As the BESS market expands globally, what are some of the main challenges faced by developers in new geographies?

In addition to North America and other experienced markets in Central and Western Europe, we are currently seeing significant investment and growth in energy storage in markets like MENA, Chile and Eastern Europe.

Brazil is ramping up to be a key growth market in the next few years: its first battery auction is coming up in April this year targeting approximately 8 GWh of capacity and it is expected to follow in the footsteps of more mature markets.

In 2025, Bulgaria installed almost 2,500 MWh of new energy storage capacity, a 1,100% increase from the previous year, making it the European Union’s fastest-growing market for BESS. This number is expected to grow in 2026.

Romania is hot on Bulgaria’s heels when it comes to BESS growth, and it is slowly but surely becoming one of the most attractive storage markets in the bloc. The country recently improved its BESS regulatory framework by eliminating double taxation of stored energy, strengthening the case for investment into BESS.

It's great news to see BESS growing at scale. But developers are facing the same growing pains that those in mature markets faced before them.

While there are experienced contractors who are familiar with the needs of a BESS project, demand can easily outstrip supply. Developers may be faced with the choice of opting for delays, waiting for the most experienced contractors to become available, or alternatively having to settle for less experienced, tier 2 contractors. Many contractors will have recently started working on renewable energy and energy storage projects, which, combined with the lack of product homogenisation in the BESS space, can cause significant errors that turn into big and costly problems in the long run. Our data at TMGX tells us that the most common causes of loss on BESS projects are due to contractor error and defective workmanship.

As insurers, it’s our job to collaborate and share the BESS underwriting and claims knowledge we’re rapidly building to the benefit of project stakeholders. We are here to help the BESS market scale sustainably as it starts to fulfil its potential as a core component of resilient energy grids worldwide.